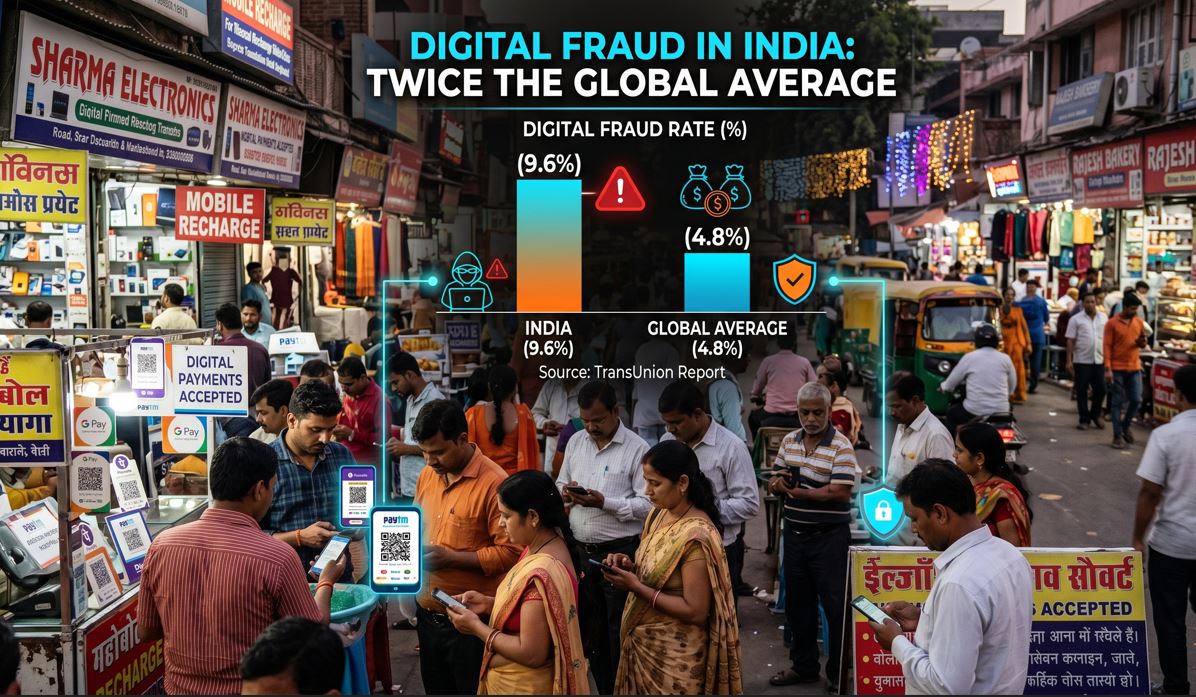

New Delhi, June 17 (UDN): India is witnessing an alarming rise in digital fraud, with the rate of suspected online fraud attempts reported to be nearly twice the global average, according to a recent report by TransUnion. The findings have raised concerns over the growing sophistication of cybercriminals and the increasing vulnerability of digital transactions.

Representational image

The report highlights that as digital adoption continues to expand rapidly across sectors such as banking, e-commerce, financial services, and telecommunications, fraudsters are also leveraging advanced technologies and social engineering techniques to target consumers and businesses.

Experts attribute the surge in digital fraud to the widespread use of online platforms, increased digital payments, and the growing volume of personal data shared through internet-based services. Common forms of fraud include phishing attacks, identity theft, account takeovers, fake investment schemes, and financial scams conducted through social media and messaging applications.

The report underscores the need for stronger cybersecurity measures, robust identity verification systems, and greater public awareness to counter emerging digital threats. Industry experts have advised users to exercise caution while sharing personal information online, verify suspicious communications, and adopt multi-factor authentication to safeguard their accounts.

The findings come at a time when India is experiencing unprecedented growth in digital transactions and internet usage, making cybersecurity a critical component of the country's digital transformation journey. Stakeholders have called for closer collaboration between government agencies, financial institutions, technology companies, and consumers to strengthen fraud prevention mechanisms and enhance digital trust.

As cyber threats continue to evolve, the report serves as a reminder of the importance of digital vigilance and the need for continuous efforts to protect users in an increasingly connected world.